Comprehensive Health Coverage: No Copays/Deductibles, PPO Network/Any doctor: $225.6/Month

Get a Quote for Health Insurance Coverage in Under 5 Minutes

How soon are you considering to purchasing health insurance?

What type of health insurance coverage do you currently have?

What's your full name?

What's your state and zip code?

What's your household income?

What's your age?

Thanks Timothy, your quote is ready!

Super Coverage Health Quotes

Take Care of Yourself and Your Family With Affordable Health Insurance

Finding health insurance on your own can feel stressful, confusing, and expensive. That’s why we built Affordable Health Quotes — to make it simple for you to compare plans, lock in lower rates, and protect the people you love. Rest easy knowing you and your family are covered with a plan that fits your lifestyle and your budget.

The Right Health Insurance Matters

We all know health insurance is important — but it doesn’t have to feel complicated. When you work with Affordable Health Quotes, here’s what you get:

A Trusted Advocate

Our licensed agents shop policies based on your unique needs, not a one-size-fits-all approach.

Expert Guidance

We simplify confusing insurance jargon so you actually understand your coverage options.

Peace of Mind

You’ll finally breathe easier knowing you have the right plan at the right price.

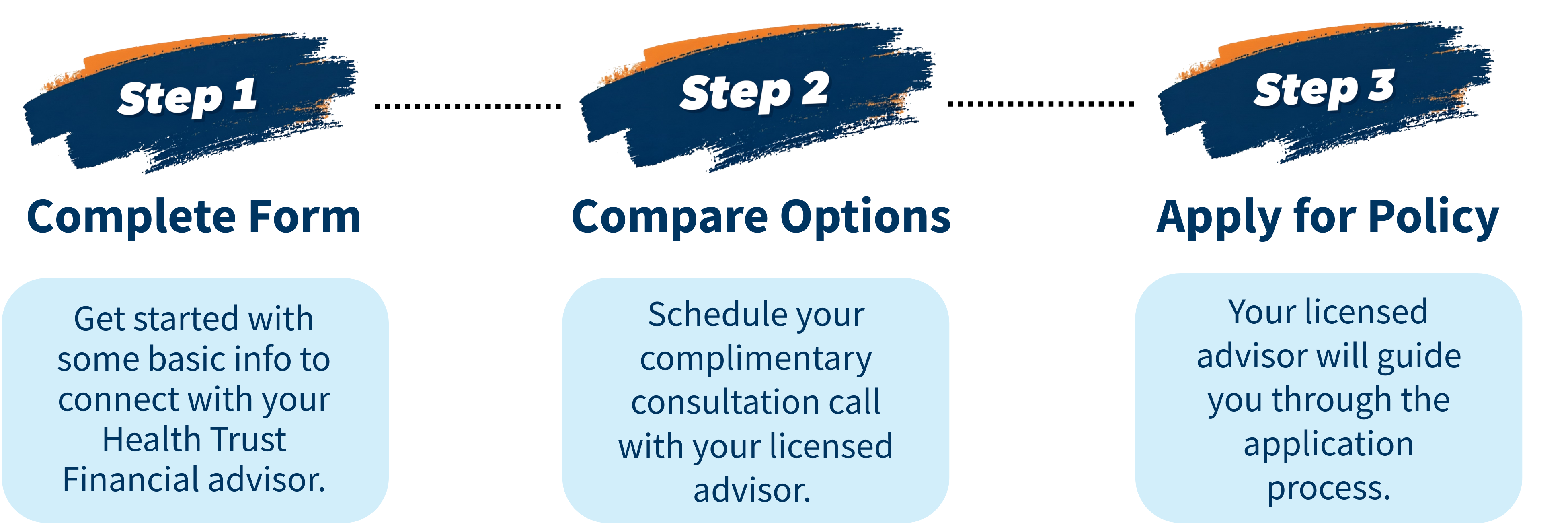

Three Simple Steps to Comprehensive Health Insurance

Who We Help

Employed but Unhappy With Your Coverage?

Not thrilled with the plan your job offers? You can shop individually and often save money.

Self-Employed, 10-99 or a Small Business Owner?

Independent contractors, freelancers, and entrepreneurs — we’ll help you navigate all your options, including marketplace plans.

Are you currently Between Jobs or Unemployed?

Losing employer coverage is tough — but there are affordable short-term and long-term options you may not know about.

Have Questions?

Health insurance is a financial protection plan that helps cover the costs of medical care, including hospital visits, surgeries, emergency treatments, routine checkups, and prescription medications. Its primary purpose is to transfer financial risk from you to the insurance company, protecting you from overwhelming medical expenses that could arise from unexpected health issues.

Everyone should have health insurance coverage. Medical emergencies and health issues can happen to anyone at any time, regardless of age or current health status. Having coverage is the most effective way to protect yourself and your family from potentially devastating medical costs.

Health insurance costs vary significantly based on several factors including your location, age, health status, the type of plan you choose, and how many family members you're covering. Individual plans typically range from several hundred to over a thousand dollars per month, while family coverage can cost significantly more.

Factors that influence your premium include your geographic area, the insurance company, plan type (HMO, PPO, etc.), deductible amount, and coverage level.

Choosing the right health insurance plan requires careful consideration of your healthcare needs and budget. Compare multiple plans and consider factors like:

- Monthly premium costs

- Deductibles and out-of-pocket maximums

- Coverage for your preferred doctors and hospitals

- Prescription drug coverage

- Specific services you might need

Working with licensed insurance professionals can help you understand your options and find coverage that meets your specific needs and budget.

You pay a monthly premium to keep your policy active. When you receive medical care, you or your healthcare provider submits a claim to your insurance company. Depending on your plan structure, you'll typically pay costs up to your deductible amount, after which your insurance begins sharing costs through coinsurance until you reach your out-of-pocket maximum.

The insurance company negotiates rates with healthcare providers, often securing lower costs than you would pay without coverage.

You can obtain health insurance through several channels:

- Employer-sponsored group plans

- Government marketplace websites

- Directly from insurance companies

- Licensed insurance brokers and agents

- Healthcare sharing ministries

- Short-term coverage options

Open enrollment is the designated period when you can sign up for new health insurance or make changes to your existing coverage. For most marketplace plans, this occurs annually in the fall. However, you may qualify for special enrollment periods if you experience qualifying life events such as marriage, job loss, moving, or having a baby.

Premiums: The monthly amount you pay to maintain your health insurance coverage.

Deductibles: The amount you must pay for healthcare services before your insurance begins to share costs.

Copays: Fixed amounts you pay for specific services (like doctor visits) regardless of whether you've met your deductible.

Coinsurance: The percentage of costs you pay after meeting your deductible, until you reach your out-of-pocket maximum.

Common types of health insurance plans include:

- HMOs (Health Maintenance Organizations): Lower costs but require you to use network providers

- PPOs (Preferred Provider Organizations): More flexibility to see any provider, with lower costs for in-network care

- High-Deductible Health Plans (HDHPs): Lower premiums with higher deductibles, often paired with Health Savings Accounts

- Short-term plans: Temporary coverage for gaps between other insurance

- Catastrophic plans: Low premiums with very high deductibles, mainly for emergency protection

A Health Savings Account is a tax-advantaged savings account available to people with qualifying high-deductible health plans. You can contribute pre-tax dollars to pay for eligible medical expenses, and unused funds roll over year to year. HSAs offer triple tax benefits: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Self-employed: You can purchase individual health insurance through the marketplace, directly from insurers, or work with licensed agents to find suitable coverage options.

Unemployed: You may qualify for COBRA continuation coverage from a previous employer, Medicaid, or special enrollment periods on the marketplace. Short-term health insurance might also be an option for temporary coverage gaps.

The federal penalty for being uninsured was eliminated, but some states still impose their own requirements and penalties. More importantly, the real risk of being uninsured is facing substantial medical bills that could create financial hardship in the event of an accident or serious illness.

© Copyright 2026. Affordable Health Solutions LLC. All Rights Reserved.